Innovation in Sustainability-Linked Model Fuels Booming Demand

Innovation in Sustainability-Linked Model Fuels Booming Demand

Directrice, Finance durable

Magali Gable a rejoint l’équipe de Finance durable de BMO au début de 2020. Elle dessert les clients de BMO dans les secteurs de l’&e…

Magali Gable a rejoint l’équipe de Finance durable de BMO au début de 2020. Elle dessert les clients de BMO dans les secteurs de l’&e…

VOIR LE PROFIL COMPLET-

Temps de lecture

-

Écouter

Arrêter

Arrêter

-

Agrandir | Réduire le texte

Disponible en anglais seulement

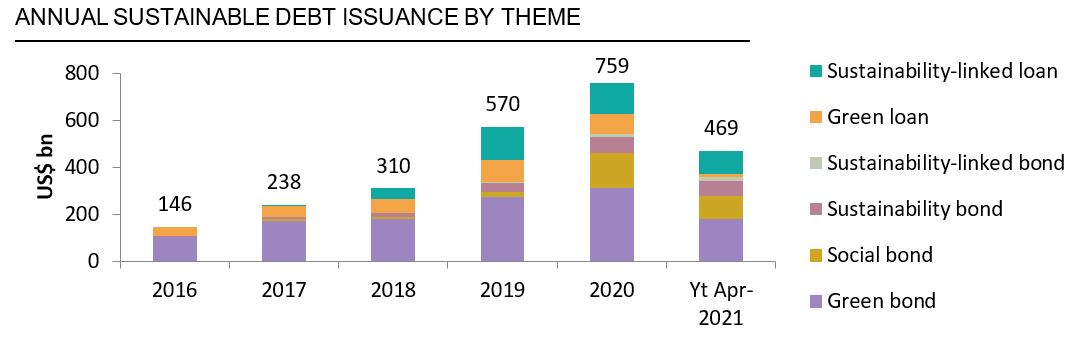

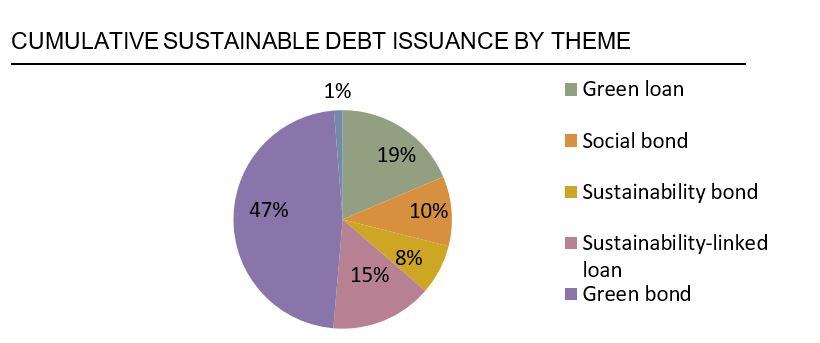

Unstoppable. That’s one word that might describe the recent growth in the sustainable debt market. Driven by its most recent innovation - the so-called sustainability-linked model - the sustainable debt market now exceeds US$2.8tn of issuance across various instruments, eclipsing the US$1tn of issuance that was so trumpeted in the green bond market last year.

Addressing a Market Gap

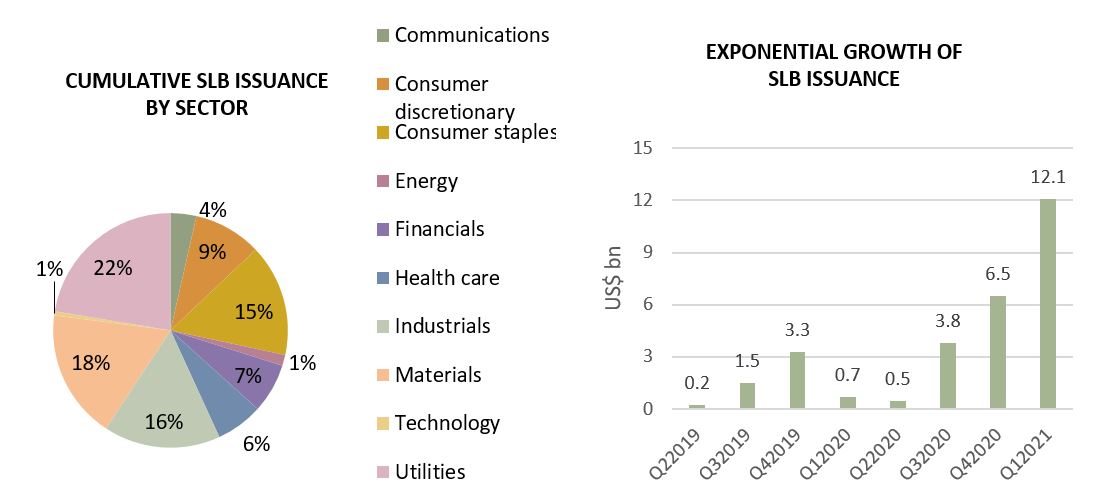

Shortly after the publication of the Sustainability-Linked Bond (“SLB”) Principles in June 2020 (see below) by the International Capital Market Association (“ICMA”), the sustainable debt market witnessed a rocketing number of issuances of those new instruments, reaching US$35.5bn1 as of April 30, 2021 across a wide range of issuers and industries - 65 issuers over 10 industries - evidencing both strong market appetite and acceptance for this new innovative asset class2. The EMEA region has been leading the charge (as it is with sustainable debt in general), with US$24.8bn of issuances, however AMER and APAC regions are following with US$7.33bn and US$3.38bn of issuances, respectively.

The reason for innovation to turn its focus on the development of the sustainability-linked bond asset class is rooted in the need to address a market gap and potential limitations of the Green/Social and Sustainability bonds model. This incredible growth is bolstered by the desire of a broader base of issuers to signal their sustainability strategies and level of commitment to the investment community in an environment where transition taxonomies around the globe are stalling and markets have yet to arrive at a unanimously agreed upon definition of transition. As a result, the sustainability-linked bond market has mirrored the adoption success of the sustainability-linked loan, its cousin in the bank market that has itself roared from 45 issuers in 2018 to 350+ global issuers these days, with a market size of US$422.6bn1 as of April 2021.

The flexibility offered by the bond format, which does not require a dedicated ‘green’ or ‘social’ use of proceeds in the way that traditional Green, Social or Sustainability bonds do, has proven appealing to corporate bond issuers. Indeed, the SLB can be used for general corporate purposes and is meant to motivate the issuer to greater sustainability as a forward-looking instrument. As a result, while the traditional use of proceeds bonds (green/social/sustainability) were pioneered by SSAs, they are so far absent in an SLB market that is dominated by Corporates.

Built-in Incentives Demonstrate Corporate Sustainability Strategy

As an increasing number of corporates establish sustainability commitments and targets that encompass a broad range of issues (with the most popular being decarbonization at large), some have doubled down by tying those to financial outcomes built into sustainability-linked bonds.

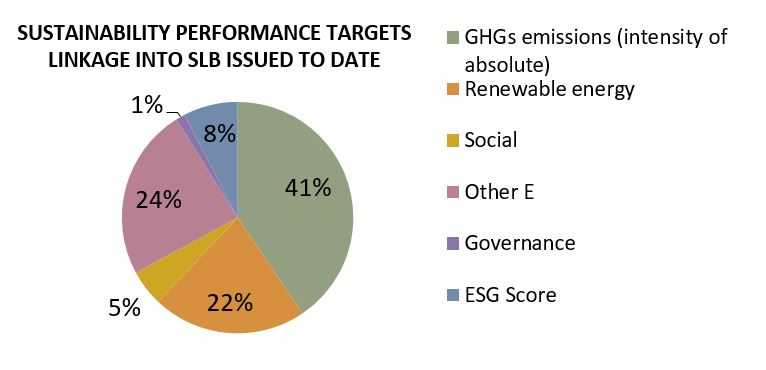

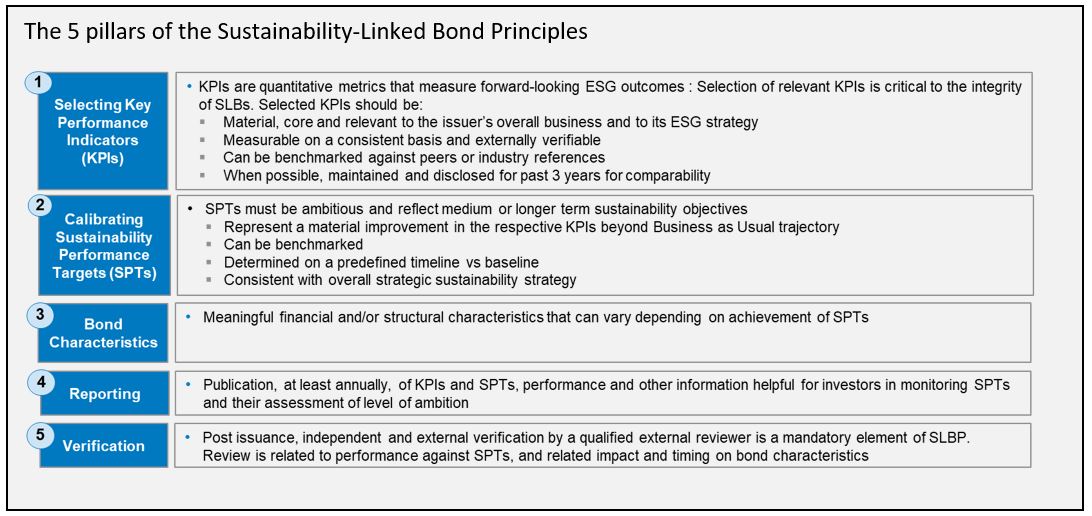

A sustainability-linked labelled bond implies that either a financial or structural characteristic of the bond will vary depending on achieving pre-agreed Sustainability Performance Targets by a certain date within the life of the bond.

Effectively, in cases where the issuer does not achieve the set targets, most of the US$35.5bn SLBs issued in the market have an interim coupon, step-up feature built into the bond, ranging from 25 to 75bps, possibly spread across several Sustainability Performance Targets. For example, Constellium SE’s US$500mm SLB executed in February of this year will experience a 12.5 basis points coupon step-up in the event that the first sustainability performance target of 25% reduction in GHG emission intensity is not achieved by December 31, 2025, and another 12.5 basis points coupon step-up in 2026 in case of failure to achieve the second 10% increase in recycled aluminum input target. Where the company is successful achieving its targets, the bond characteristics won’t change.

Innovative alternative penalties approaches have also emerged, ultimately supporting achievement of the issuer’s sustainability strategy. In LafargeHolcim’s EUR 850mm SLB transaction executed in November 2020, for example, the 75bps potential coupon step-up could be donated to a research institute active in the fields of climate research or climate change mitigation, or reallocated internally to an R&D budget dedicated to cement decarbonization. In Etihad’s US$600mm SLB deal in October 2020, failure to achieve its decarbonization target at the target observation date would not trigger a coupon step-up but instead an obligation to buy carbon offsets.

While we expect further innovation in the bond incentive structure and alternate pay-off mechanisms, we foresee limited investors’ appetite to accept coupon step-down in the case of successful achievement of the sustainability performance target – whereas this has been market practice in the bank market for sustainability-linked loan instruments.

Materiality, Ambition and Transparency

For investors, SLBs also provide greater visibility into the overall sustainability strategy of the issuer, and help drive diversification in labelled bonds portfolios with a broadening of the range of issuers, geographies and industries beyond the traditional, often low-yield green bond market, including sustainability-linked bond issuances from high yield issuers (e.g. EUR 500mm Public Power Corp.’s SLB, carrying a higher coupon of 50 bps if it fails to reduce its CO2 emissions by 40% by December 2022 from 2019 levels). That said, some investors have yet to participate in the SLB market, citing difficulty assessing the calibration of sustainability targets, reconciling bond impacts or other practical challenges into portfolio inclusion.

A core element of the SLB is whether the Key Performance Indicators (“KPI”) are material for the business and whether the targets are set at a level that is ambitious enough and beyond business-as-usual. To opine on such, the market relies again on a critical part of the integrity of sustainable finance: TRANSPARENCY. For the market to thrive, transparency is critical to explaining the materiality of the KPI, the targets comparability and ambition as well as context within the issuer’s strategy and broader industry.

Beyond ICMA’s guidelines on KPI materiality, there is also a lot of discussion in the market on the concept of proportionality regarding the amount raised in consideration to potential investments needed to achieve the sustainability targets as well as calibration of the potential coupon step-up in connection with the ambition level or bond pricing. Considering the still nascent state of the SLB market, those discussions are meant to and will evolve overtime as more issuances come to market and a “critical mass” is reached.

As with the “use of proceeds” bond market, the new kid on the block will gain further acceptance and earn increased credibility as a function of issuer transparency and integrity around their sustainability ambitions and progress trajectory. Despite potential challenges, the SLB can be regarded as an important signalling and financing tool in the sustainable finance toolbox, and help issuers telegraph their sustainability strategy and demonstrate related goals.

Evolving Menu of Sustainability Options

Overall, evolving investors’ expectations have contributed to product innovation and deployment of a “menu” of sustainable debt options to finance their sustainability objectives or demonstrate various ESG commitments. The acceleration in standardization in 2020 with the publications of new standards along with enforcement of regulations have enhanced the market and the volume of new issuances of sustainability-linked products is expected to continue its ascension over the coming quarters – including potentially for some sectors adopting a combined format with the traditional use of proceeds model as we’ve seen with two sustainability-linked green bonds issued in March.

1 As per BNEF

2 Including European Central Bank accepting SLBs as central bank collaterals since January 2021